Do Junior-Mining Press Releases Move the Stock?

Junior mineral explorers are unusual companies. Most of them never pull anything out of the ground. They are pre-revenue, often trading for a few cents a share, and their whole value is a story about what might be sitting under a patch of dirt in Texas or northern Ontario. The way that story reaches the market is the press release: "drilled 12.5 g/t gold over 8 metres," "closes $5M financing," "options the Whatever Creek property." So here is a fair question. When one of these companies puts out a release, does the stock actually move? By how much? And does the bump stick, or does it fade?

One note before we start: this is research and storytelling, not investment advice. It is also not a study. Bird's 2013 paper, which I lean on below, was a proper peer-reviewed study; this is a quick, not-especially-robust web scrape written up as a blog post. If it nudges someone toward the rigorous version, a real follow-up to Bird on the TSX, it will have done its job.

We are not the first to ask

This question was first asked by Bird, Grosse and Yeung (2013), in the Australian Journal of Management, who ran a proper event study on mining exploration, resource, and reserve announcements among juniors listed on the ASX. An event study is just a way of measuring how a stock reacts to a piece of news, after stripping out everything else that was moving that day. Their findings, which I checked against:

- About a +1.5% jump on the announcement day.

- A reversal afterwards: the pop fades over the following weeks, and most of all in the smallest companies.

- Roughly 40 to 50% of the move happens before the announcement is public, which is consistent with information reaching the market ahead of the formal release.

- Companies that used positive adjectives in the headline got bigger reactions.

I'm not aware whether this has been done on Canada's TSX Venture and CSE, which, alongside the ASX, are where most of the world's junior explorers list. So that was the gap I went after.

The data, all of it free

No Bloomberg terminal here. The whole thing runs on public, free sources.

- The company list: the TMX public company directory, about 1,400 TSX Venture issuers, of which roughly 820 are mining or exploration outfits.

- The press releases: Newsfile, TMX's newswire and the main distributor for junior-mining news. The web scraper found about 700 mining companies and pulled their full release archives, more than 36,000 dated press releases going back to 2013.

- The stock prices: Yahoo Finance, daily data, adjusted for splits.

- The benchmarks: the S&P/TSX Venture Composite index, to subtract out "the whole junior market moved today," plus gold, silver, and copper futures.

That last point does most of the work. A gold explorer's stock jumping 8% the day it reports drill results means nothing if gold itself rose 5% and the whole sector was green. The method's job is to isolate the abnormal return, the part that is actually about this company's news, and not the market or the metal. Get that wrong and you will fool yourself.

The pop is real

Across about 9,900 cleanly measured events from 2013 to 2026, the answer to "do press releases move the stock?" is a clear yes.

A press release produces about a +1.6% abnormal return on the announcement day, and that is after subtracting both the market and the commodity. The effect is statistically significant at any conventional threshold.

The size is the interesting part. Bird and co-authors found about +1.5% on the ASX, a decade earlier and a hemisphere away. The Canadian junior market does very nearly the same thing. That is a clean replication, and replication is rarer than it should be. (Again, not peer-reviewed).

The content of the release matters too, in a way that makes sense once you see it. Ranked by the size of the day-zero pop:

- A permit granted: about +3.9%.

- A deal (an acquisition, joint venture, or option): about +3.2%.

- "We are going to drill," or drilling has started: about +2.4%.

- Actual drill results: about +1.4%.

- A financing: about +1.2%.

- An economic study, meaning a PEA or feasibility report: roughly 0%.

Two of these stand out. "We are going to drill" beats "here is what we drilled" (+2.4% against +1.4%), so the market pays more for anticipation than for the result itself, which is exactly the pattern Bird flagged. And the big, expensive economic studies get almost no reaction at all, because by the time a project reaches feasibility, the market has long since priced it in. Bird found the same thing for reserve announcements.

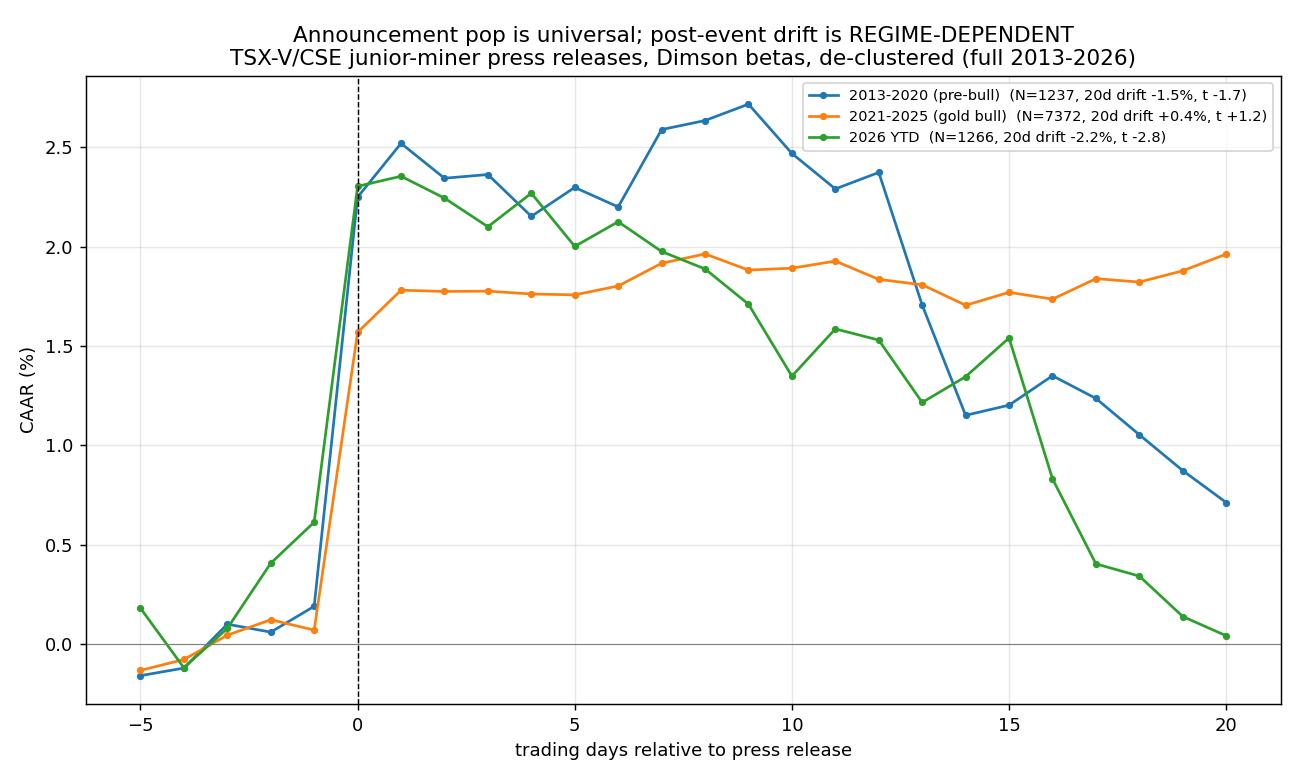

The twist: the fade is real too, but only sometimes

Here is where it got interesting. Bird's headline result was that the pop reverses, with juniors giving the gain back over the following weeks. My first few passes said the opposite. No reversal in Canada, the pop just sits there. I nearly wrote that up as the finding.

Then I stress-tested my own work with a batch of adversarial checks, and one of them caught a mistake I had introduced. I had limited the price data to the last five years, so my study was really only looking at 2021 to 2026, which happens to be a sustained gold bull market. In a bull market everything drifts up, and that upward drift quietly buries the fade.

Fix the mistake, pull the full history, and the real picture appears. The announcement pop is universal. It shows up in every period, and is actually a bit bigger (+2.3%) in the calmer years before 2021. But the post-announcement fade depends on the market regime:

- 2013 to 2020 (no bull market): pop, then a fade of about 1.5%.

- 2021 to 2025 (gold bull market): pop, then flat.

- 2026 so far: pop, then a fade of about 2.2%, and statistically real.

So Bird's reversal does happen on Canadian juniors. It just hides during bull markets. The rising tide of 2021 to 2025 lifted the fades up into flatness, and as soon as the tide went out (the years before 2021, and now 2026) the reversal came back. That is a more honest answer than either "reversal" or "no reversal" on its own, and I only got to it because I did not trust my first result.

Two caveats, because honesty is the point

Survivorship. My company list is made of today's survivors. The juniors that blew up and delisted, the ones that almost certainly fell hardest after their last hopeful press release, are not in the data at all. About a third of the tickers had no price history left to pull. So the real fade is probably worse than what I measured, not better.

A red herring I had to retract. One pass showed financings producing a suspicious positive drift of about +2.7%. The stress-test took it apart. The typical financing actually drifts slightly down, which is what theory predicts, since issuing new shares dilutes the existing ones. The +2.7% was a handful of survivors that went on to do very well, dragging the average up. That is survivorship bias again. Name it, and the +2.7% disappears.

So can you trade it?

Short answer: no, and this is not advice to try. The pop is real, but it lands right at the announcement (and Bird's "about half of it is already priced in" holds here too), it is smaller than the 5 to 15% bid-ask spread you would pay to trade these illiquid names, and the one pattern that looks exploitable, fading the pop in non-bull markets, would require shorting micro-cap juniors. That is very hard to do in practice, and expensive when it is possible at all. The edge disappears the moment you account for the cost of capturing it.

Where the result is genuinely useful is the other direction, for the companies writing the releases. There is a real, measurable order to what moves a stock (deals and permits and "we are drilling soon" ahead of raw results, with feasibility studies barely registering), and clearer, more substantive releases tend to go with cleaner market reactions. That is a story about how the news is written, not about getting rich.

The point for this blog

The finding I would have published after a weekend, "Canadian juniors don't reverse the way the Australians do," was wrong. And it was wrong because my window was too short. What saved it was not me being clever. It was a process that challenges my own conclusions before believing them: re-run on split samples, re-run across market regimes, re-test the timing, audit the labels, and go looking specifically for the artifact. That is the part worth keeping.

Data: the TMX company directory, Newsfile, and Yahoo Finance, all public and free, covering 2013 to 2026. Method: an event study with thin-trading-adjusted betas (Dimson, 1979) and event-induced-variance-robust inference (Boehmer, Musumeci and Poulsen, 1991), de-clustered so that overlapping releases are not double-counted. Benchmark: the S&P/TSX Venture Composite plus gold, silver, and copper futures. Primary reference: Bird, Grosse and Yeung (2013), Australian Journal of Management 38(2). None of this is investment advice.

Attack your own answers.